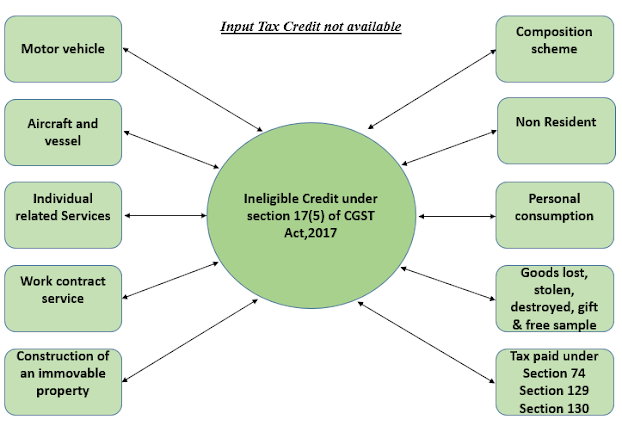

Sometime the Goods or services which are supplied by a registered taxpayers are returned by the purchaser due to certain reasons like deficient value or quantity. As a result, taxpayers

get confused in these types of transactions w.r.t to GST treatment. For such transactions the GST laws has the provision of Debit and Credit Notes.

For

the removal of confusion or better understanding we have explained about the

credit and debit notes in detailed

manner and in tabular form.

|

Particulars

|

Credit

Note

|

Debit

Note

|

|

Section

|

Section 34(1)

of CGST Act, 2017

|

Section 34(3)

of CGST Act, 2017

|

|

Meaning

|

Where a tax invoice issued for

supply of any goods or services or both and the following situation occurs: - Value of tax charged in the tax invoice is

found to exceed the taxable value

or tax payable; or

- Where the goods are returned by the recipient;

or

- Where

the goods or services or both supplied are found to be deficient,

Then, in the above cases, the registered person may issue a credit note to the recipient.

|

Where a tax invoice issued for

supply of any goods or services or both and the following occurs: - Value of tax charged in the tax invoice is

found to be less than the taxable

value or tax payable; or

- Where the goods or services or both supplied

are found to be excessive,

Then, in the above cases, the

registered person may issue a credit note to the recipient.

|

|

Who is liable to issue

|

Supplier who has supplied any goods or services or both

|

Supplier who has supplied any goods or services or

both

|

|

Time limit for issue

|

Earlier of :

Due date return for the month of September or,

Date of furnishing the annual return

|

No time limit has been defined under GST Act but it should be issue

or before the due date of the return for the month of September so that recipient

will be eligible to take the input tax credit for the same.

|

|

Adjustment by Supplier

|

Supplier who has issued the credit note shall declare

such credit note in the return (GSTR-1) for the month during which such

credit note has been issued and adjust his tax liability accordingly.

|

Supplier who has issued the Debit note shall declare

such Debit note in the return (GSTR-1) for the month during which such Debit

note has been issued and pay his tax liability accordingly.

|

|

Adjustment by Recipient

|

Recipient has to adjust the input tax credit in GSTR-3B with the

amount of the Credit note in the the

month in which credit note has been received.

|

Recipient has to avail the input tax credit in GSTR-3B with the

amount of the Debit Note in the the

month in which debit note has been received but not

later than from the due date for the month of September.

|

|

Interest by the recipient

|

If the recipient has not adjusted the credit note

with his input tax credit in the same month in which it has been issued, he

is liable to pay the interest due to excess claim of input tax credit under

section 50 of CGST Act, 2017.

|

If the recipient has not availed the input tax

credit until the due date of return for the month of September, credit shall

lapse and he will not be eligible to take the benefit of the debit note.

|

|

Record

|

Supplier has to maintain the records for all the credit notes until

the expiry of 72 months from the date of furnishing of annual return

|

Supplier has to maintain the records for all the credit notes until

the expiry of 72 months from the date of furnishing of annual return

|

|

Format

|

There is no prescribed format. However the credit

note issued by a supplier must contain the following particulars, namely: - Name, address and Goods and Services Tax

Identification Number of the supplier;

- Nature of the document;

- A consecutive serial number not exceeding

sixteen characters, in one or multiple series, containing alphabets or

numerals or special characters hyphen or dash and slash symbolised as “-” and

“/” respectively, and any combination thereof, unique for a financial year;

- Date of issue;

- Name, address and Goods and Services Tax

Identification Number or Unique Identity Number, if registered, of the

recipient;

- Name and address of the recipient and the

address of delivery, along with the name of State and its code, if such

recipient is un-registered;

- Serial number and date of the corresponding

tax invoice or, as the case may be, bill of supply;

- Value of taxable supply of goods or services,

rate of tax and the amount of the tax credited to the recipient; and

- Signature or digital signature of the supplier

or his authorized representative.

|

There is no prescribed format. However, the debit

note issued by a supplier must contain the following particulars, namely: - Name, address and Goods and Services Tax

Identification Number of the supplier;

- Nature of the document;

- A consecutive serial number not exceeding

sixteen characters, in one or multiple series, containing alphabets or

numerals or special characters hyphen or dash and slash symbolised as “-” and

“/” respectively, and any combination thereof, unique for a financial year;

- Date of issue;

- Name, address and Goods and Services Tax

Identification Number or Unique Identity Number, if registered, of the

recipient;

- Name and address of the recipient and the

address of delivery, along with the name of State and its code, if such

recipient is un-registered;

- Serial number and date of the corresponding

tax invoice or, as the case may be, bill of supply;

- Value of taxable supply of goods or services,

rate of tax and the amount of the tax debited to the recipient; and

- Signature or digital signature of the supplier

or his authorized representative.

|

The above has been explained with the following example:

Credit Note:

On

15.05.2020, Vikram (supplier) sold the 500 units of X product for Rs 10,000/-@ 18% GST to Shyam (Recipient) and

later on, the following deficiency or errors were noted:

Case-1

Bill raised for 600 units amounting Rs 12,000/-

Case-2

Tax charged @ 28%

Case-3

Goods returned by Shyam on 01.06.2020

Treatment:

|

Case

|

Supplier(Vikram)

|

Recipient

(Shyam)

|

|

Case-1

|

- Issue credit note for 100 units amounting

Rs.2,000/-

- Adjust the liability in the same month return.

- Maintain record for the credit note till 72

months from the date of the annual return.

|

- Record the credit note issued by the supplier in his books.

- Adjust the input tax credit in the GSTR-3B for the month for which credit note relates.

|

|

Case-2

|

- Issue credit note for entire Invoice and raise a fresh invoice with 18% GST.

- Adjust the liability in the same month return.

- Maintain record for the credit note till 72

months from the date of the annual return.

|

- Record the Credit note and Invoice issued by the supplier in his books.

- Adjust the input tax credit in the GSTR-3B for

the month for which credit note relates.

|

|

Case-3

|

- Issue credit note for Rs 10,000/- and GST at 18%.

- Adjust the liability in the same month return

- Maintain record for the credit note till 72

months from the date of the annual return.

|

- Record the Credit note issued by the supplier in

his books.

- Adjust the input tax credit in the GSTR-3B for

the month for which credit note relates.

|

Debit Note:

On 25.05.2020, Saytam (supplier) supplied is 100 Kg of Y Product for Rs 5,000/-@ 18% to Naresh

(Recipient) and later

on the following deficiency or errors were noted:

Case-1 Bill raised for 80Kgs amounting Rs 4,000/-

Case-2

Tax charged @ 12%

Treatment:

|

Case

|

Supplier(Satyam)

|

Recipient

(Naresh)

|

|

Case-1

|

- Issue Debit note for 20kg amounting Rs.1,000/-

- Pay the liability in the same month return

- Maintain record for the credit note till 72

months from the date of the annual return.

|

- Record the Debit note issued by the supplier in

his books.

- Avail the input tax credit in the GSTR-3B for

the month for which debit note relates.

|

|

Case-2

|

- Issue Debit note against the original invoice with zero taxable value but containing the tax amount i.em for 6% (18%-12%).

- Pay the liability in the same month return

- Maintain record for the Debit note till 72

months from the date of the annual return.

|

- Record the Debit note issued by the supplier in

his books.

- Avail the input tax credit in the GSTR-3B for

the month for which debit note relates.

|

Important points:

Credit and debit notes are always issued by the

supplier and also filed by the supplier in his GSTR-1.

Buyer can avail/adjust the input tax credit

based on the hard/soft copy of the debit/credit note received from the supplier and it will be

reflected in his GSTR-2A.

There is no time limit defined for issuing the debit

note under the GST Act, but the supplier has to issue the debit note or before the due date of

return for the month of September, so that the recipient can avail the input tax credit as per

Section 16(4) of CGST Act, 2017.

If the Recipient has not adjusted his input tax

credit related to Credit note in the month in which credit note has been issued, he is liable to pay

interest under section 50 of CGST Act, 2017.

If the Supplier has not paid the output tax

related to debit note in the month in which the debit note has been issued, he is liable to pay

interest under section 50 of CGST Act, 2017.

For information regarding liability not reported or input not availed for the last financial year must read

----------------------------------------------------------------------------------------------------------------------------

For any tax related issues/queries:

Please Contact:

Tax Tunnel

📱 +91-78382 12620

Comments

Post a Comment